How might tomorrow's banks say less and do more? How might they find greater meaning in people's lives and be culturally relevant, connecting at a human level whilst avoiding patronising imagery and stories?

The global banking industry seems to suffer the Boiling Frog Syndrome in terms of changing its behaviour. Powerful forces are reshaping its future, but can they see it and react quickly enough? From customer expectations, to technology, to regulatory requirements, the list is considerable on how customers relate to and interact with bank brands. New market entrants are redefining how people view and interact with banking services.

We always associate banks and their brands with the High Street retail experience. They try to portray a warm personality with community service and trust at their heart, yet underlying these generic apple-pie-messages is an undertow of customer distrust from harder times. Conventional banks are being seduced with the desire to be shiny and forward-thinking at one end, but are countered by dusty legacies of traditional branches and their inefficiencies at the other end. Only for some, the category is enjoying one of the most exciting periods of its history due to game-changing digital technologies.

When you view this from a customer's perspective, it becomes increasingly clear that the consumer experience and the brand interface is being diminished. Massive technological change is having transformational effects across virtually all consumer services.

The old rules do not apply anymore, so banks cannot expect to regain trust by engaging in clichéd campaigns and claiming to be “on your side”. Most of us have grown tired of the one-way conversation where we are told how we should feel or how a bank is going to look after us and our families.

Can banks say less and do more by way of experiential brand activities? Less of a monologue and more of a two-way relationship with people? Financial products have been challenged by the emergence of apps, which are a kind of “do-it-yourself” financial product in themselves. They are disruptors during a time of general cynicism.

In a climate obsessed with process improvement, I'd love to be a fly on the wall when it comes to deciding marketing strategies.

There is the big risk megabanks will fail to align with their true brand objectives of customer wants and expectations. In order to build trust again, banks must forge a new meaningful relationship with people by becoming an active, trusted advisor genuinely interested in people's lives and businesses and providing relevant guidance and assistance in an everyday way. Of course, they say these things in their advertising, but do they do them? The customer belief gap has to be closed before all the warm advertising has any real effect, and it can only happen when the product experience is seamless and easy.

I suspect that the legal departments kill off every lovely bit of lyricism in the creative engagement process. Finding new ways of having relevance in the hearts and minds of people requires prodigious amounts of outside-in thinking. Most banks—in my observation—are simply not nimble enough in communicating with the archetypes they serve.

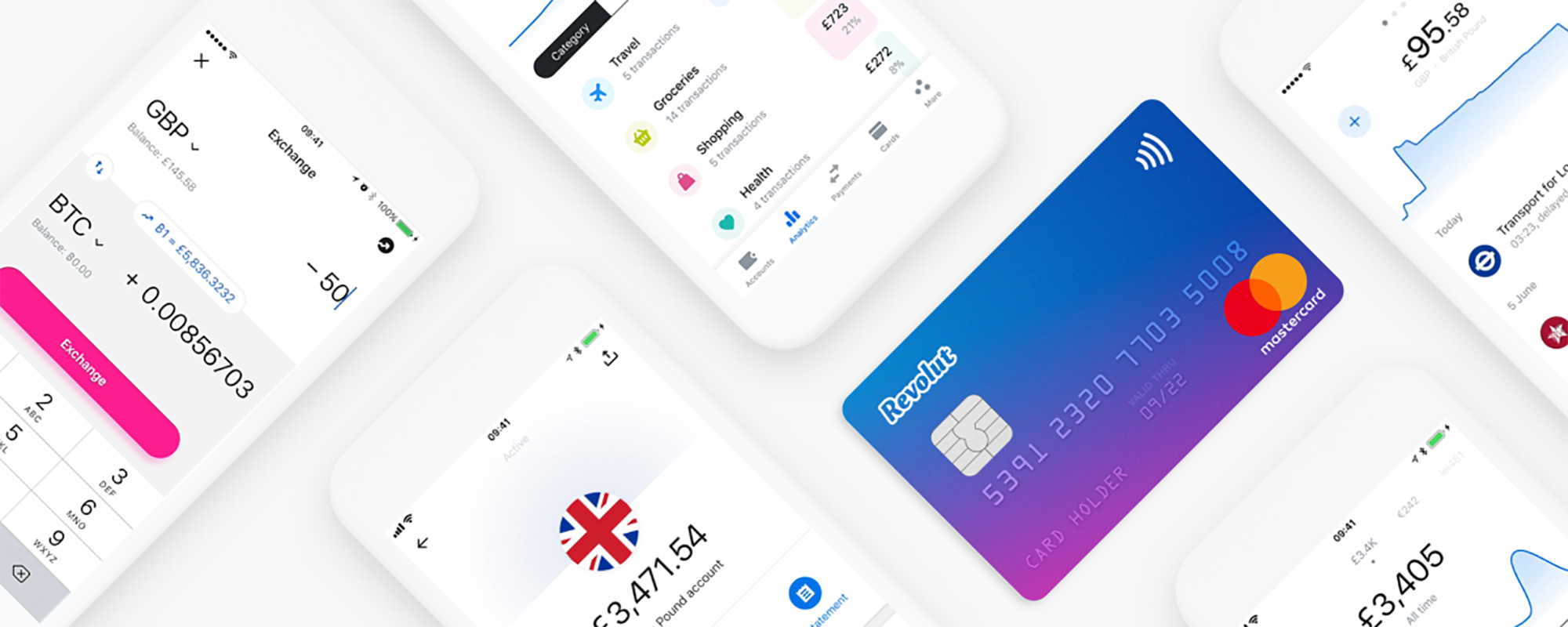

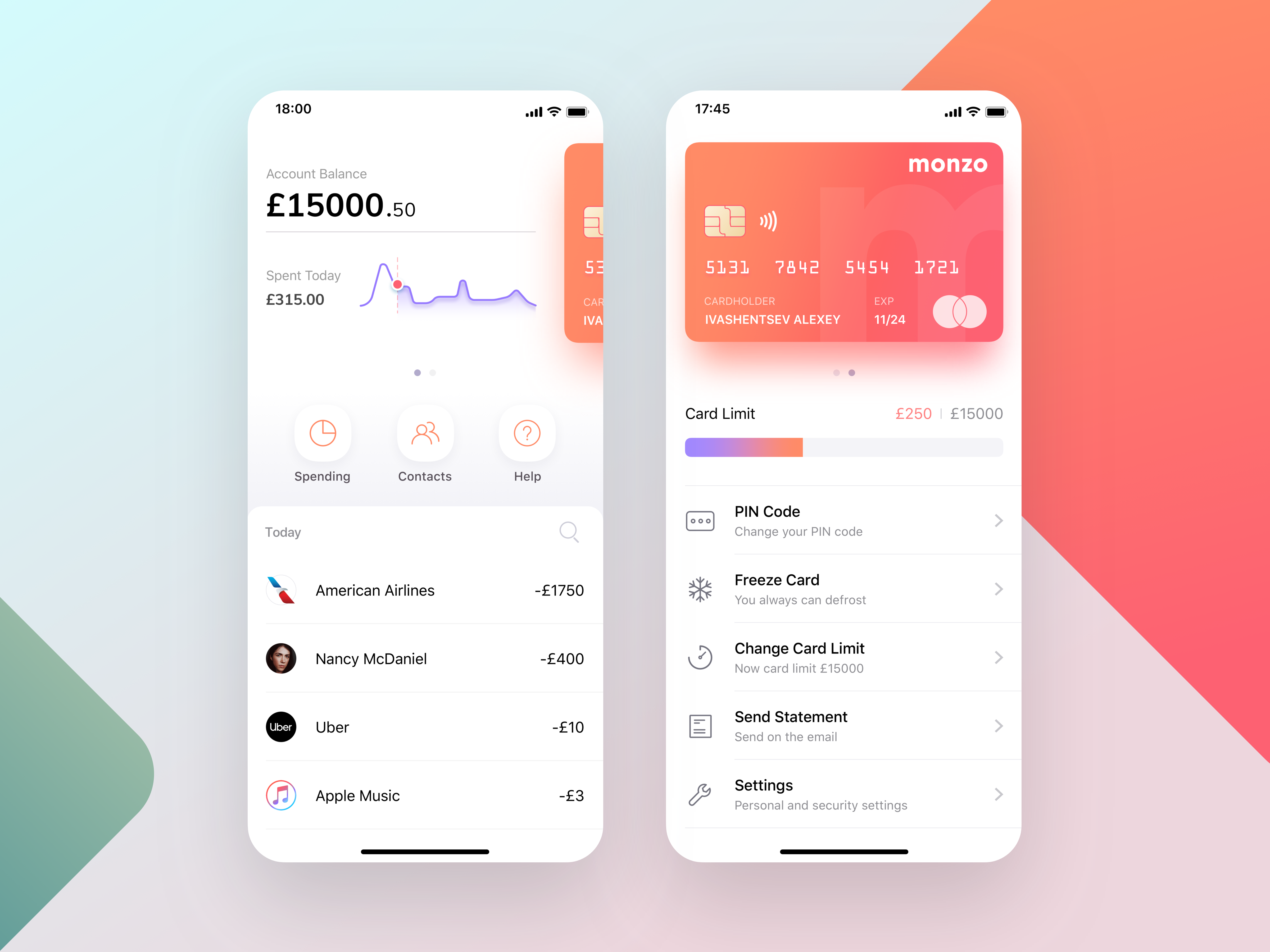

Take Revolut which is coming to New Zealand very soon. They’ve entered the market leveraging "customer-centric ease" so well, with lower transactional fees and foreign-exchange rates to name a few of the bells and whistles. Beautifully simple and intuitive interfaces make their product so easy to use. Monzo is another exciting product in the same sector. Here we see two companies with traditional products, but without the traditional structures and the accompanying hang-ups. Short and snappy, these brands are both well-named, coupled with minimalistic design and a marvellous expectation of simplicity.

Engaging product experiences open your eyes and encourage you to budget more carefully, with greater ease. This is human-centred design at its best. Standing in the customer's shoes is such an overused statement these days.

If you truly understand the customer journey—the feelings people have when they use your product—you should be guided by human instinct. “What would I want that would make my life easier and more convenient?” Once that's established, the challenge is to seamlessly deliver it through meaningful branding, language, UI and UX design.

Most of these new products we are seeing are currently limited to foreign exchange and current account banking. I think it can only be a matter of time before they move into other products such as savings, business banking, and mortgages.

My read is that many of the banks are putting internal innovation teams together which are constantly changing with co-opted people. Internally, if one is destined to an innovation team of this kind, it seems to have become the kiss-of-death career-wise.

I'm not suggesting external consultants are the total answer either. You need to create internal champions with the authority to make change.

I've been in so many workshops coaching people who are full of enthusiasm and rightfully so, in that they have discovered insights by standing on street corners with us. Yet when confronted with senior management who view the material in the boardroom, design thinking becomes design blinking. Impassive seniors with unmoved faces look at anecdotes on walls, rapidly blinking in disbelief.

Shifting this belief takes enormous courage, yet we see the outcome in the banking world of brilliant young companies who will eclipse the large disbelieving ‘blinkers’ very quickly.

One potential obstacle that banks may experience in shaping this new future is how their internal departments are currently organised and relate to each other. Traditionally the marketing department had the responsibility of shaping their relationship with and understanding the customer. However in recent years the key customer interface is more likely to be a website or phone screen. When a technology department of the business is creating a digital product for customers, the skill set and knowledge base of the marketing department should help form the product experience, however this is often not the case.

They must meet in the middle for best results. In contrast, new entrants to the banking market do not have this inter-department complication as optimal product experience is the primary goal from the outset. Perhaps a new department function should form to help resolve this tension. A Chief Experience Officer for example who could bridge the gap. As well as creative agencies that are at the nexus of art and technology – agencies that are equipped to create these consumer-focused experiences. Human-centred but tech-enabled.

Banks in particular are reducing their physical footprint within most high streets and are now “meeting” more of their customers online. The challenge now is how might they create a sense of community in the virtual world? Within a few years, I imagine that transactional facilities will be very small, so how will banks evolve and retain the current presence within our communities? With the movement of brands like Apple shifting into financial products, it will be interesting to see how their slick marketers will interpret community engagement. I can imagine that in the years ahead, you will describe your bank as a companion as opposed to a company. “MyApple” would be a good start wouldn't it?

Perhaps there will be a day when parents with their teenage children learn how to manage their finances through cooking demonstrations at the bank. For instance, I could envision a wonderful joint community venture between our client Fisher & Paykel Appliances and the Bank of New Zealand. Now there's a "blinking moment" in a banker’s boardroom.